Why Financial Literacy Still Holds Back Gambian Entrepreneurs

ANALYSISINSIGHTS

Walking through any Gambian market, from Banjul to Basse, you'll see businesses everywhere. Women balance baskets of fresh produce on their heads, while food vendors line the sides of the road.

Behind all this hustle lies a problem that quietly kills growth: financial illiteracy. Yes, entrepreneurship is booming here. However, many Gambians lack the financial knowledge to sustain or scale what they're building. Financial literacy, knowing how to plan, budget, save, invest, and borrow wisely, remains one of the least understood yet most critical tools for success.

The Knowledge Gap Is Real

Most Gambian entrepreneurs start small. They use personal savings or get help from family. Almost none begin with any training in financial management. The result? Many operate informally, with no proper record-keeping and little understanding of cash flow.

Field interviews and local business studies show that a huge portion of small enterprises in The Gambia run without written accounts. Business owners calculate profits in their heads, mixing business income with personal spending. This makes it nearly impossible to track how they're doing or plan for what's next.

Consider a tailor in Bundung who produces dozens of outfits every week. She buys fabric, pays helpers, covers electricity costs—but can't tell you how much she actually earns after expenses. Without clear records, her pricing might be too low to keep the business alive. This isn't unique to her. It's a pattern you'll find across small enterprises here.

Getting Money Isn't the Same as Managing It

Access to finance is still a dream for many entrepreneurs. Banks and microfinance institutions regularly reject loan applications because of missing documentation or weak business plans. Even worse? Those who do secure funding often misuse it.

A local finance officer put it bluntly:

"Some business owners use their loan money for weddings, school fees, or personal shopping instead of investing in the business. When repayment time comes, they're stuck in debt."

This happens because people don't understand interest rates, repayment terms, or the concept of reinvestment. What should be an opportunity becomes a burden. Financial literacy isn't just about getting money; it's about knowing what to do with it once you have it.

The Informal Economy Trap

The informal sector employs over two-thirds of Gambia's working population. It provides jobs and income, sure. But it also keeps entrepreneurs isolated from formal systems that encourage accountability and financial discipline. Most transactions happen through verbal agreements with little documentation. Many entrepreneurs prefer cash over digital payments, viewing banks as complicated or intimidating. Some actively avoid formalizing their operations because they fear taxation.

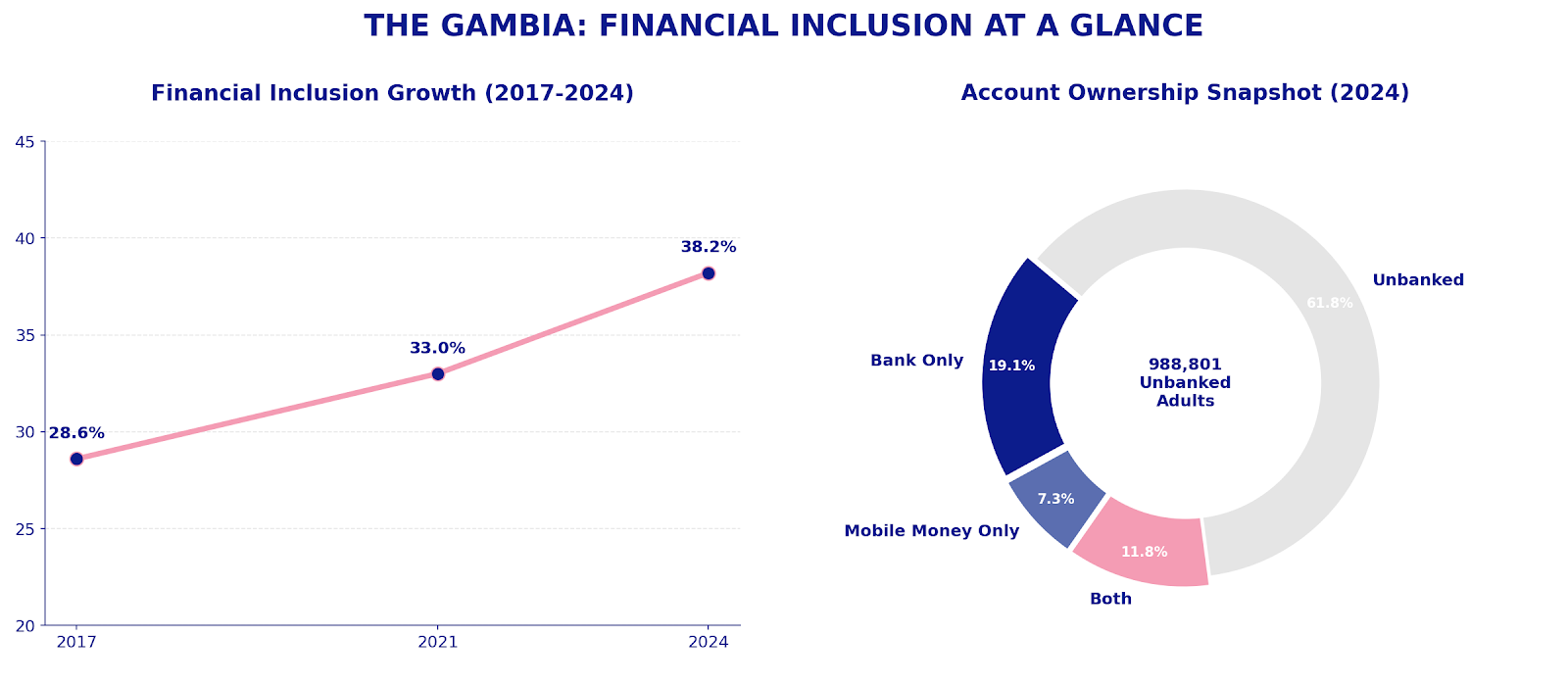

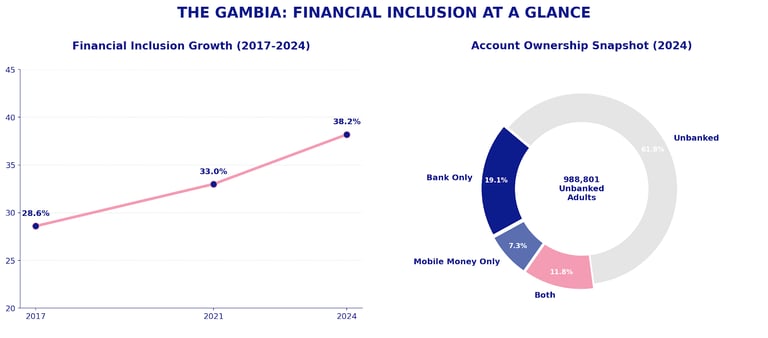

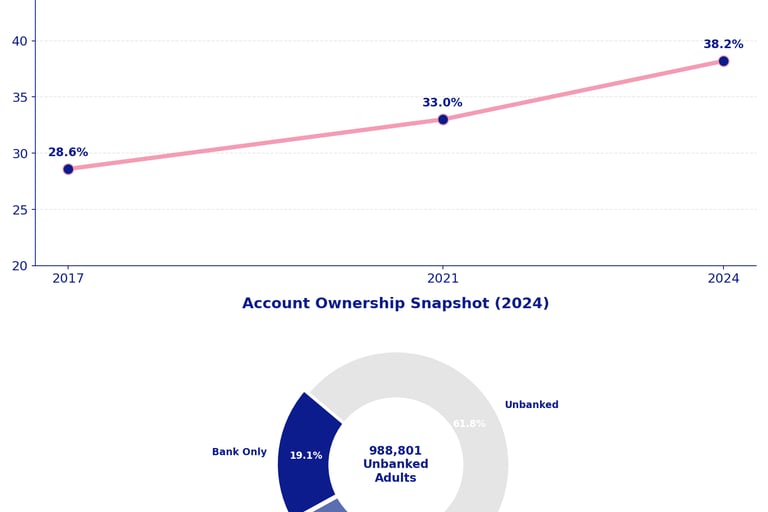

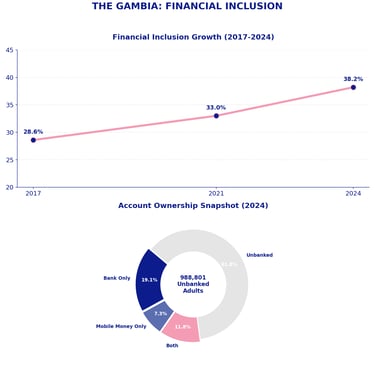

Figure: Financial inclusion in The Gambia (2024). This graph shows the distribution of account ownership among adults in The Gambia. It uses the World Bank’s Global Findex definitions, where an “account” may be held at a formal financial institution (bank or similar) or through a mobile money provider. The share of unbanked adults, those without any formal account type, remains high, highlighting the need for greater financial literacy and access.

A fruit seller in Serekunda Market told me, "I don't trust banks. I'd rather keep my money where I can see it."

That mindset reflects a deeper cultural barrier. Training programs can't just teach financial skills—they have to build trust and show relevance first.

Why Current Programs Aren't Working

Several organizations have launched entrepreneurship and financial management programs—from the Gambia Investment and Export Promotion Agency (GIEPA) to various youth-led initiatives. The problem? Most reach only a tiny fraction of the population.

Workshops are often conducted in English, scheduled during business hours, or designed by people who don't understand the day-to-day reality of local traders. For real impact, financial education needs to leave the classroom and meet entrepreneurs where they actually are: in markets, workshops, and online spaces.

What Needs to Change

Closing the financial literacy gap requires both government and private institutions to completely rethink their approach. Here's what would actually work:

Integrate financial literacy into education. Schools, colleges, and vocational centers need to include basic money management and entrepreneurship in their standard curriculum. When young people learn these skills early, they gain confidence in making financial decisions later.

Teach in local languages. Many entrepreneurs are more comfortable learning in Mandinka, Wolof, or Fula. Programs that use local examples and languages make complex financial concepts actually stick.

Leverage media and mobile tools. Radio programs, community outreach, and mobile apps can spread financial knowledge effectively. With platforms like Africell Money and QCell Money growing fast, there's a real opportunity to teach entrepreneurs how to save and track expenses digitally.

Build mentorship networks. Successful business owners should mentor others in their communities. Peer learning builds trust and gives people practical knowledge they can use immediately.

Simplify banking partnerships. Financial institutions need to make loan processes clearer, explain interest rates in plain language, and actually educate clients before handing them money. When entrepreneurs understand how credit works, repayment improves, and businesses become sustainable.

The Bottom Line

Financial literacy isn't a luxury. For Gambian entrepreneurs, it's a lifeline. Without it, hardworking, skilled, determined people stay trapped in cycles of debt and uncertainty. But when you give entrepreneurs financial knowledge, you give them the power to make informed choices, plan, and grow with real confidence.

The Gambia's economic transformation won't come from aid packages or policy documents alone. It will come from citizens who understand how to manage and multiply their resources wisely. If we make financial literacy a national priority, The Gambia won't just produce more entrepreneurs. We'll build sustainable businesses that create jobs, reduce poverty, and drive lasting economic growth.